All Categories

Featured

[/image][=video]

[/video]

This can cause less advantage for the policyholder compared to the financial gain for the insurance policy firm and the agent.: The pictures and assumptions in advertising and marketing products can be deceptive, making the policy appear a lot more attractive than it may in fact be.: Be conscious that monetary advisors (or Brokers) gain high commissions on IULs, which could influence their referrals to offer you a plan that is not suitable or in your benefit.

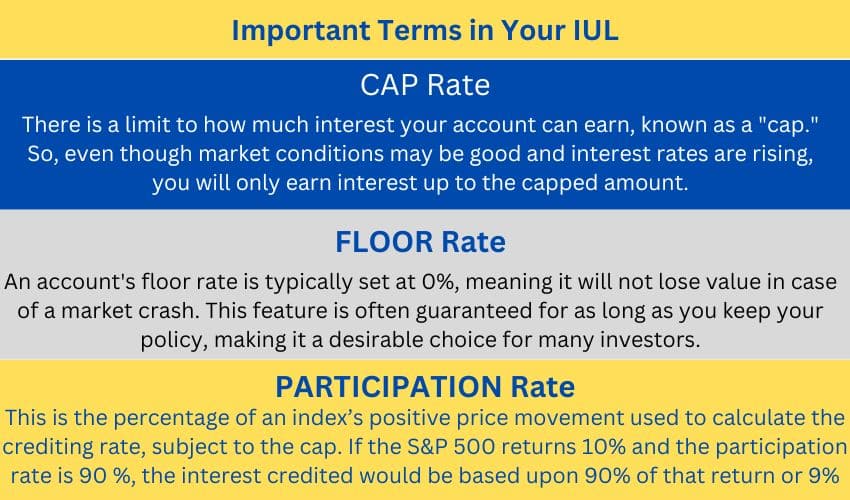

Most account options within IUL products assure among these limiting aspects while allowing the various other to drift. One of the most common account alternative in IUL policies features a floating annual interest cap in between 5% and 9% in existing market conditions and a guaranteed 100% involvement rate. The passion earned amounts to the index return if it is less than the cap however is covered if the index return exceeds the cap rate.

Various other account choices may consist of a drifting participation price, such as 50%, without any cap, implying the interest credited would certainly be half the return of the equity index. A spread account credits rate of interest above a drifting "spread out rate." If the spread is 6%, the passion credited would certainly be 15% if the index return is 21% however 0% if the index return is 5%.

Rate of interest is normally credited on an "yearly point-to-point" basis, suggesting the gain in the index is determined from the factor the premium entered the account to specifically one year later on. All caps and engagement prices are after that applied, and the resulting passion is credited to the policy. These prices are changed annually and used as the basis for determining gains for the following year.

Instead, they utilize choices to pay the rate of interest guaranteed by the IUL contract. A telephone call choice is a monetary contract that gives the choice customer the right, but not the responsibility, to acquire a possession at a specified price within a particular time period. The insurance provider purchases from a financial investment bank the right to "get the index" if it exceeds a certain level, called the "strike price."The carrier might hedge its capped index obligation by purchasing a phone call option at a 0% gain strike rate and composing a telephone call option at an 8% gain strike cost.

Index Universal Life Insurance Review

The spending plan that the insurer has to buy options depends upon the yield from its general account. If the service provider has $1,000 internet premium after reductions and a 3% yield from its basic account, it would certainly designate $970.87 to its general account to grow to $1,000 by year's end, making use of the staying $29.13 to buy choices.

This is a high return assumption, showing the undervaluation of alternatives out there. Both biggest variables affecting floating cap and involvement prices are the returns on the insurance business's basic account and market volatility. Providers' basic accounts primarily include fixed-income assets such as bonds and home loans. As returns on these properties have actually declined, service providers have had smaller sized allocate acquiring choices, causing lowered cap and involvement prices.

Providers commonly highlight future performance based upon the historical efficiency of the index, applying existing, non-guaranteed cap and engagement prices as a proxy for future performance. However, this method might not be reasonable, as historic projections often reflect higher previous rate of interest and assume constant caps and involvement prices in spite of diverse market conditions.

A much better strategy might be alloting to an uncapped engagement account or a spread account, which entail acquiring reasonably inexpensive options. These strategies, however, are less stable than capped accounts and might call for constant adjustments by the provider to show market conditions precisely. The narrative that IULs are conventional items supplying equity-like returns is no longer sustainable.

With practical assumptions of alternatives returns and a reducing allocate buying alternatives, IULs might offer marginally greater returns than typical ULs yet not equity index returns. Possible purchasers must run pictures at 0.5% over the interest rate attributed to standard ULs to evaluate whether the policy is appropriately moneyed and qualified of providing promised efficiency.

As a trusted companion, we collaborate with 63 top-rated insurance provider, guaranteeing you have accessibility to a varied series of alternatives. Our services are entirely cost-free, and our expert consultants provide objective recommendations to help you locate the most effective coverage customized to your requirements and budget plan. Partnering with JRC Insurance coverage Group means you get customized service, affordable prices, and comfort understanding your monetary future remains in qualified hands.

Life Insurance Indexed Universal Life

We aided hundreds of households with their life insurance policy requires and we can aid you as well. Written by: Louis has actually remained in the insurance policy organization for over three decades. He concentrates on "high risk" instances in addition to even more complicated protections for long-term treatment, handicap, and estate preparation. Expert evaluated by: High cliff is a qualified life insurance policy representative and one of the proprietors of JRC Insurance policy Group.

In his spare time he enjoys spending quality time with family, traveling, and the outdoors.

Variable plans are underwritten by National Life and dispersed by Equity Services, Inc., Registered Broker/Dealer Associate of National Life Insurance Coverage Firm, One National Life Drive, Montpelier, Vermont 05604. Be sure to ask your economic advisor about the lasting care insurance policy's attributes, advantages and premiums, and whether the insurance policy is proper for you based on your economic scenario and objectives. Handicap earnings insurance coverage usually supplies regular monthly revenue advantages when you are incapable to work due to a disabling injury or ailment, as defined in the policy.

Cash money value grows in an universal life policy via credited interest and reduced insurance coverage expenses. If the policy lapses, or is given up, any type of outstanding impressive lendings taken into consideration in the policy plan be subject to ordinary common taxesTax obligations A repaired indexed universal life insurance coverage (FIUL)plan is a life insurance product item provides you the opportunity, when adequately sufficiently, to participate get involved the growth development the market or an index without directly straight spending the market.

{kind=link}

Latest Posts

Ameritas Iul

Index Universal Life Vs Term Life Insurance

Nationwide Iul Accumulator Review